There are two important changes in the Central Excise side, which I would like to bring to your special attention: 3.1.1 Excise...

There are two important changes in the Central Excise side, which I would like to bring to your special attention:

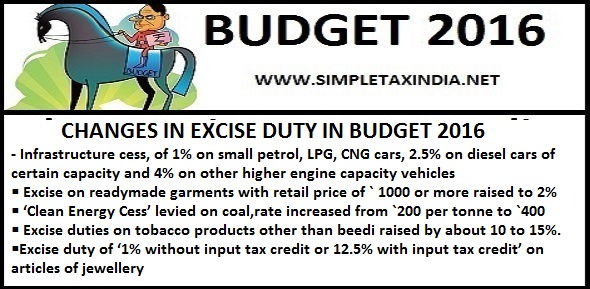

3.1.1 Excise duty of 2% (without CENVAT credit) or 12.5% (with CENVAT credit) is being levied on readymade garments and made up articles of textiles falling under Chapters 61, 62 and 63 (heading Nos. 6301 to 6308) of the Central Excise Tariff except those falling under 6309 and 6310 of retail sale price (RSP) of Rs.1000 and above when they bear or are sold under a brand name. This optional levy would apply to such readymade garments and made up articles of textiles regardless of the composition of the garment / article. However, in respect of readymade garments and made up articles of textiles other than those mentioned above, the optional levy of „Nil (without CENVAT credit) or 6% (with CENVAT credit)‟ in case of garments / articles of cotton, not containing any other textile material and „Nil (without CENVAT credit) or 12.5% (with CENVAT credit)‟ in case of garments / articles of other composition, as the case may be, shall continue. The tariff value for readymade garments and made up articles of textile is also being increased from 30% to 60% which shall apply to all goods mentioned in the notification No.20/2001-CentralExcise (N.T.) dated 30.04.2001. It may be noted that the new levy is similar to the levy of mandatory excise duty of 10% on readymade garments and made up articles of textiles [goods falling under Chapters 61, 62 and 63 (heading Nos. 63.01 to 63.08)] when they bear or are sold under a brand name, which was introduced in the Budget 2011-12, except that:

a.

The present levy is an optional

levy, that is domestic manufacturers will have the option to pay excise duty of

„2% (without CENVAT credit) or 12.5% (with CENVAT credit)‟,

b. The levy

is restricted to such articles which have RSP of Rs.1000 and above, and

c. The

tariff value is being revised from 30% of RSP to 60% of the RSP.

3.1.2

In this regard, I would like to

reiterate the instructions issued vide Budget letter F.No.334/3/2011-TRU dated

28.02.2011, Instruction D.O. F.No.334/3/2011-TRU, dated 04.03.2011 and

Instruction D.O. F.No. B-1/3/2011-TRU, dated 25.03.2011. The said instructions

shall apply mutatis mutandis to the new levy. Salient features of these

instructions [suitably modified for the proposed optional levy, as underlined]

are as under:

(i)

The levy shall not apply to

retail tailoring establishments that stitch garments in a customized manner to

the size and style specifications of individual customers, whether out of

fabric purchased by the customer from the same establishment or

fabric

supplied by the customer.

(ii)

The brand name owner, who gets the

goods manufactured on his own account on job work, shall pay the duty leviable

on such goods as if the goods were manufactured by him. The brand name owner

(and not the job-worker) shall be required to register and comply with all the

provisions of Central Excise law. Rule 4 (1A) of the Central

Excise Rules, 2001 and Para 1, clause (vi) of notification

No.36/2001-C.E. (N.T.), dated 26.06.2001 refers.

(iii)

However, the brand name owner

will be given the option to authorise his job-worker to pay the duty leviable

on the goods. If such an authorisation is given, then the job-worker would have

to obtain registration. Proviso to rule 4 (1A) of the Central Excise Rules,

2001 and proviso to Para 1, clause (vi) of notification No.36/2001-C.E. (N.T.),

dated 26.06.2001 refers.

(iv)

A unit which manufactures goods

bearing the brand name of another person out of inputs or raw materials which

have been purchased independently and not supplied by the brand owner, does not

satisfy the definition of “job-worker” and would, therefore,

have to

obtain registration and discharge the duty liability.

(v)

In cases where the brand name

owner gets goods bearing its brand manufactured from other manufacturers

(normally small units) without providing the raw materials or inputs, and if

the RSP is not affixed or marked on such goods when they are cleared in the

course of sale from the factory of a manufacturer to the brand owner, then no

excise duty would be payable by such a manufacturers since the RSP of such

goods is not disclosed to them by the brand owner. However, since the process

of labeling or re-labelling constitutes a process of “manufacture”, duty on the

tariff value (based on the RSP) would be payable as and when the brand owner

labels the goods with the RSP of Rs.1000 or above and clears them for further

sale.

(vi) The value for computing the eligibility as well as the exemption limit for purposes of SSI exemption would be the tariff value of the goods. Explanation (C) to notification No.8/2003-C.E., dated 1st March, 2003 refers.

(vii) The SSI exemption for the month of March, 2016 will be Rs.12.5 lakh, subject to fulfilment of other conditions of the notification No.8/2003-C.E., dated 01.03.2003.

For this purpose, notification No.8/2003-C.E., dated 1st March, 2003 is being amended suitably.

(viii) The eligibility for availing of the SSI exemption in 2015-16 for the month of March 2016 is that the value of clearances for home consumption from one or more manufacturer from one or more unit should not have exceeded Rs. 4 crore in the financial year 2014-15. The computation for this purpose shall be done in accordance with the provisions of Para 3A of notification No. 8/2003-C.E. For this purpose, a certificate from a Chartered Accountant based on the books of accounts for 2014-15 shall suffice.

(ix) Excisable goods which were produced on or before 29.02.2016 but lying in stock as on 29.02.2016 shall attract excise duty upon clearance. Manufacturers shall keep a stock declaration of finished goods, goods-in-process and inputs as on 29.02.2016 in their records duly certified by a Chartered Accountant so as to enable the manufacturers to claim CENVAT credit on inputs or inputs contained in goods lying in stock as already provided for in Rule 3(2) of the CENVAT Credit, Rules, 2004, if he so desires. No stock declaration, will, however, be required to be made to the jurisdictional central excise authorities.

(x) Full exemption from Central Excise duty will be available to duty-paid goods returned to the manufacturer during a financial year up to an aggregate ceiling not exceeding 10% of the value of clearances for home consumption made in the preceding financial year. The manufacturer would be required to observe the following procedure for this purpose:

(a) To submit an intimation within 48 hours of the receipt of the returned goods about the value of returned goods received in his factory/registered premises;

(b) To maintain proper accounts/record of the receipt, finishing operations, and dispatch of returned stock indicating the monthly and cumulative value of the returned stock received during the financial year and to produce the same as and when required.

Notification No. 31/2011-C.E., dated 24th March, 2011 refers. This facility has been provided since it is a common practice in this industry that the duty-paid stock cleared to the wholesale dealer/retailer on consignment basis that remains unsold is returned to the manufacturer either at the end of the season or from time to time. Such returned goods are cleared either as such or after „re-finishing‟ operations to another wholesaler or retailer for sale (often at reduced prices). The re-finishing operations could involve cleaning, ironing, re-folding, repacking or relabeling, some of which constitute “manufacture” in terms of the relevant Chapter Notes. This facility obviates the need to pay excise duty twice on the same goods.

3.2.1 Excise duty of 1% (without CENVAT credit) or 12.5% (with CENVAT credit) is being levied on articles of jewellery [excluding silver jewellery, other than studded with diamonds/other precious stones] with a higher threshold exemption upto Rs. 6 crore in a year and eligibility limit of 12 crore. Thus, a jewellery manufacturer will be eligible for exemption from excise duty on first clearances upto Rs. 6 Crore during a financial year, if his aggregate domestic clearances during preceding financial year were less than Rs. 12 crore. In other words, jewellery manufacturer having aggregate value of clearances in a financial year exceeding Rs. 12 crore, will not be eligible for this threshold exemption in the subsequent financial year. Necessary amendments have been made in notification No.8/2003-Central Excise, dated 01.03.2003 in this regard.

3.2.2 The SSI exemption for the month of March, 2016 for jewellery manufacturers will be Rs.50 lakh, subject to the condition that value of clearances for home consumption from one or more manufacturer from one or more factory or premises of production or manufacture during the financial year 2014-15 should not be more than Rs. 12 crore. Computation for this purpose shall be done in accordance with the provisions of Para 3A of notification No. 8/2003- CE. For this purpose, a certificate from a Chartered Accountant, based on the books of accounts for 2014-15, shall suffice.

3.2.3 Similarly, for determining the eligibility for availing of the SSI exemption from 2016-17 onwards, a certificate from a Chartered Accountant, based on the books of accounts for 2015-16, shall suffice.

3.2.4 Excisable goods which were produced on or before 29.02.2016 but lying in stock as on 29.02.2016 shall attract excise duty upon clearance. Jewellery manufacturer shall keep a stock declaration of finished goods, goods-in-process and inputs as on 29.02.2016 in their records duly certified by a Chartered Accountant so as to enable the manufacturers to claim CENVAT credit on inputs or inputs contained in goods lying in stock as already provided for in Rule 3(2) of the CENVAT Credit, Rules, 2004, if he so desires. No stock declaration, will, however, be required to be made to the jurisdictional central excise authorities.

3.2.5 Further, the following simplified procedure and guidelines are being issued for strict compliance:

i. Registration once applied for shall be granted within two working days, along with simplified registration procedure as prescribed under Notification No. 35/2001-CE.

ii. Further, the requirement of post registration physical verification of the premises has been also done away with in this case. Necessary amendments have been made to Notification No. 35/2001-CE for this purpose.

iii. Moreover, documents being maintained by the jewellery manufacturers for State VAT or Bureau of Indian Standards (in the case of hallmarked jewellery) shall suffice for Excise purposes also.

iv. The private records of the jewellery manufacturers, giving details of daily stock for his own purposes, shall be accepted for the purposes of Rule 10 of the Central Excise Rules 2002.

v. A notification, providing for an optional centralized central excise registration for jewellery manufacturers with centralized billing or accounting system is being issued under Rule 9 (2) of the Central Excise Rules, 2002.

vi. Also, jewellery manufacturers will be eligible for a simplified return applicable for optional excise duty of 1%/2% without CENVAT credit under notification No.1/2011-CE, under Rule 12 of the Central Excise Rules, 2002.

vii. Rule 12AA of the Central Excise Rules, 2002 provides that in case of goods falling under chapter heading 7113, every person (not being an EOU or SEZ unit) who gets jewellery made from any other person, and supplies the raw materials such as gold/silver/gemstones to the job-worker for such manufacture, the duty liability would be on such person who gets articles of jewellery made from the job worker. In such cases, the principal manufacturer (and not job worker) will be required to get Central Excise registered, pay duty and follow other compliance requirements. This will ensure that small artisans/goldsmiths are not required to take any excise registration.

viii. The levy is based on self-assessment and therefore, no physical visits shall be made to registered units in the normal course.

4. I would like to emphasise that the Board desires that all necessary steps shall be taken to enable the new taxpayers to comply with these new levies without any difficulty. The thrust of these new levies shall be voluntary compliance. Therefore, visits to such units should not be made in the normal course. These instructions may be disseminated to the field formations for strict compliance.

5. Difficulties faced, if any, in implementation of these new levies which are not covered by the instructions issued in this regard may be communicated to the Board without delay.

6. In order to achieve a sharper focus, I have alluded only to the key highlights of the budgetary changes in this communication. The details are contained in the Finance Bill and notifications which alone have legal force. My team and I have made every possible effort to avoid the occurrence of errors or mistakes in the Budget documents. However, given the scale of changes, inadvertent errors cannot be ruled out. I shall be grateful if the provisions of the Finance Bill and notifications are studied carefully and feedback on issues that may need clarification is provided urgently.

EXCISE

Chapter 1 to 20: No change.

Chapter 21:

1) Basic Excise Duty is being increased on pan masala [2106 90 20] from 16% to 19%. S.No.35 of notification No.12/2012-Central Excise dated 17th March, 2012 as amended by notification No.12/2016-Central Excise dated 01.03.2016 refers. Accordingly, the duty leviable under the compounded levy scheme has also been modified. Notification No. 30/2008 – Central Excise (N.T.) dated 01.07.2008 as amended by notification No. 9/2016-Central Excise (N.T.) dated 01.03.2016 and notification No.42/2008-Central Excise dated 01.07.2008 as amended by notification No.17/2016-Central Excise dated 01.03.2016 refer.

Chapter 22:

1) Excise duty on “waters, including mineral waters and aerated waters, containing added sugar or other sweetening matter or flavoured” falling under Chapter sub-heading 2202 10 is being increased from 18% to 21%. Clause 143 (i) of the Finance Bill refers. By virtue of declaration under the Provisional Collection of Taxes Act, 1931, this increase will come into force with immediate effect.

Chapter 23: No change.

Chapter 24:

1) The additional duty of excise levied under the Seventh Schedule to the Finance Act, 2005 on non-filter and filter cigarettes of sub-heading 2402 20 is being increased. Clause 231 of the Finance Bill, 2016 refers. By virtue of declaration under the Provisional Collection of Taxes Act, 1931, these changes will come into force with immediate effect. There is no change in the Basic Excise Duty leviable under the First Schedule to the Central Excise Tariff Act, 1985 and the NCCD leviable under Seventh Schedule to the Finance Act, 2001. The changes in additional duty of excise rates on cigarettes are summarized below.

Tariff Item

|

Description

|

Additional

Duty of Excise

|

|

(length in mm)

|

(Rs. per 1000

sticks)

|

||

Existing Rate

|

New Rate

|

||

2402 20 10

|

Non filter not exceeding 65

|

70

|

215

|

2402 20 20

|

Non-filter exceeding 65 but not exceeding 70

|

110

|

370

|

2402 20 30

|

Filter not exceeding 65

|

70

|

215

|

2402 20 40

|

Filter exceeding 65 but not exceeding 70

|

70

|

260

|

2402 20 50

|

Filter exceeding 70 but not exceeding 75

|

110

|

370

|

Tariff Item

|

Description

|

Additional Duty of Excise

|

|

(length in

mm)

|

(Rs. per 1000 sticks)

|

||

2402 20

90

|

Other

|

180

|

560

|

2)

Basic Excise Duty on other

tobacco products falling under heading 2402 is being increased as under:

Tariff

Item

|

Description

|

Basic Excise Duty rate

|

|

From

|

To

|

||

2402 10 10

|

Cigar and cheroots

|

12.5% or Rs.3375

|

12.5% or Rs.3755

|

per thousand,

|

per thousand,

|

||

whichever is higher

|

whichever is higher

|

||

2402 10

20

|

Cigarillos

|

12.5% or Rs.3375

|

12.5% or Rs.3755

|

per thousand,

|

per thousand,

|

||

whichever is higher

|

whichever is higher

|

||

2402 90

10

|

Cigarettes of tobacco substitutes

|

Rs.3375 per

|

Rs. 3755 per

|

thousand

|

thousand

|

||

2402 90

20

|

Cigarillos of tobacco substitutes

|

12.5% or Rs.3375

|

12.5% or Rs. 3755

|

per thousand,

|

per thousand,

|

||

whichever is higher

|

whichever is higher

|

||

2402 90

90

|

Others of tobacco substitutes

|

12.5% or Rs.3375

|

12.5% or Rs. 3755

|

per thousand,

|

per thousand,

|

||

whichever is higher

|

whichever is higher

|

||

3)

The tariff rate of Basic Excise

Duty on Paper rolled biris [whether handmade or machine made] and other biris

[other than handmade biris] [2403 19 29] is being increased from Rs.30 per

thousand to Rs.80 per thousand. However, there is no change in effective basic

excise duty rate on these goods which is presently Rs.21 per thousand.

4)

Basic Excise Duty is being

increased on unmanufactured tobacco, and jarda scented tobacco, gutkha and

chewing tobacco. Clause 143 (i) of the Finance Bill, 2016 refers. These changes

will come into effect immediately owing to a declaration under the Provisional

Collection of Taxes Act, 1931. There is no change in NCCD and Health Cess

rates. The changes in basic excise duty rates are summarized below.

Accordingly, the duty leviable under the compounded levy scheme has also been

modified. Further, the speed slabs and the deemed production and duty payable

per month on chewing tobacco without lime tube / lime pouches and jarda scented

tobacco are being aligned. Notification No. 11/2010 – Central Excise (N.T.)

date 27.02.2010 as amended by notification No.10/2016-Central Excise (N.T.)

dated 01.03.2016 and notification No. 16/2010-Central Excise dated 27.02.2010 as

amended by notification No.16/2016-Central Excise dated 01.03.2016 refer.

Commodity

|

Current rate of BED

|

Proposed rate of BED

|

|

(%)

|

(%)

|

||

Gutkha

|

70

|

81

|

|

Unmanufactured Tobacco

|

55

|

64

|

|

Chewing Tobacco

|

70

|

81

|

|

(including

filter khaini)

|

|||

Zarda

Scented Tobacco

|

70

|

81

|

|

5)

The Seventh Schedule to the

Finance Act, 2001 which provides for levy on NCCD of excise on specified goods

is being amended so as to align the tariff lines under Chapter 24 with the

First Schedule to the Central Excise Tariff Act, 1985. Relevant Clause of

Finance Bill, 2016 refers. Also, notification No. 6/2005-Central Excise dated

01.03.2005 is being amended so as to align the tariff lines under Chapter 24

with the First Schedule to the Central Excise Tariff Act, 1985. Notification

No. 6/2005-Central Excise dated 01.03.2005 as amended by notification

No.18/2016-Central Excise, dated 01.03.2016 refers.

Chapter 25 to 26: No change

Chapter 27:

1)

Oil Industries Development Cess

levied on domestically produced crude oil under the Oil Industry (Development)

Act, 1974 is being reduced from Rs.4500 PMT to 20% ad valorem. This change will

come into force with effect from the date of assent to the Finance Bill, 2016.

Till the enactment of the Finance Bill, 2016, Notification prescribing 20%

effective rate of OID Cess will be issued by Ministry of Petroleum &

Natural Gas.

2)

The Basic Excise Duty rate on

aviation turbine fuel [ATF] [2710 19 20] is being increased from 8% to 14%.

However, ATF for supply to Scheduled Commuter Airlines [SCA] from the Regional

Connectivity Scheme [RCS] airports shall attract 8%. The rate of 14% will

operate

through the

tariff and the

rate of 8%

will operate through

S. No. 77

of notification

No.12/2012- Central Excise, dated 17th March, 2012 as amended by

notification No.12/2016-Central Excise dated 1st March, 2016.

3)

The Schedule Rate of Clean Energy

Cess, levied on coal, lignite and peat, is being increased from Rs.300 per

tonne to Rs.400 per tonne. Clause 232 of the Finance Bill, 2016 refers. The

increase in rate of Clean Energy Cess will come into effect immediately owing

to a

declaration

under the Provisional Collection of Taxes Act, 1931. Accordingly, notification

No.1/2015-Clean Energy Cess, dated 1st March, 2015 is being rescinded,

vide notification No. 1/2016-Clean Energy Cess, dated 1st March, 2016 and the rate of Rs.

400 per tonne will operate through the Schedule. Further, the Clean Energy Cess

is being renamed as CleanEnvironment Cess. This change will come into force with effect from the

date of enactment of the Finance Bill, 2016.

4)

Clean Energy Cess on all goods

produced or extracted as per traditional and customary rights enjoyed by local

tribals without any license or lease in the State of Nagaland is being fully

exempted. Notification No. 5/2010-Clean energy

Cess, dated 22.06.2010 as amended by notification No. 2/2016-Clean Energy Cess

dated 1st March, 2016 refers.

Chapter 28, 29 or 38:

1)

Basic Excise Duty on

micronutrients falling under Chapter 28, 29 or 38, which are covered under Sr.

No. 1(f) of Schedule 1 Part (A) of the Fertilizer Control Order, 1985 and are

manufactured

by the manufacturers which are registered under FCO, 1985, is being reduced

from 12.5% to 6%. Notification No.12/2012- Central

Excise, dated 17th March, 2012 as amended by notification No. 12/2016- Central Excise

dated 1st March, 2016 [New S. No. 109A] refers.

Chapter 30: No change

Chapter 31:

1)

Basic Excise Duty on mixture of

fertilizers, made by physical mixing of chemical fertilizers on which

appropriate duty of excise has been paid, by Co-operative Societies, holding

certificate of manufacture for mixture of fertilizers under the Fertilizer

Control Order 1985, for supply to the members of such Co-operative Societies,

is being fully exempted. Notification No. 12/2012- Central Excise, dated 17th

March, 2012 as amended by notification No. 12/2016- Central Excise dated 1st

March, 2016 [New S. No. 128A] refers.

Chapter 32 to 33: No change

Chapter 34:

1)

S. Nos. 39 and 40 of No.

49/2008-Central Excise (N.T.), dated 21.12.2008 are being amended so as to

prescribe Retail Sale Price based assessment of excise duty on all goods

falling under heading 3401 and 3402 with an abatement of 30%. S. Nos. 39 and 40

of

notification

No.49/2008-Central Excise (N.T.), dated 21.12.2008 as amended by notification

No.

12/2016-Central Excise (N.T.) dated 1st March,

2016 refers.

The Third Schedule to the Central Excise Act, 1944

is also being amended so as to include therein all goods falling under heading

3401 and 3402. Clause 142(i) of the Finance Bill, 2016 refers. By virtue of

declaration under the Provisional Collection of Taxes Act, 1931, these changes

will come into force with immediate effect.

Chapter 35 to 37: No change

Chapter 38:

1)

Ready Mix Concrete [3824 50 10]

manufactured at the site of construction for use in construction work at such

site is being fully exempted from excise duty. Also, the expression

„site‟ is

being defined in the exemption notification. S. No. 144 of notification No.

12/2012-

Central Excise, dated 17th March, 2012 as amended by

notification No. 12/2016-Central Excise dated 1st March, 2016 refers.

Chapter 39:

1) Basic

Excise Duty on sacks and bags of polymers of any plastics is being rationalized

at

15%. Notification No.12/2012- Central Excise, dated

17th March, 2012 as amended by notification No. 12/2016- Central Excise

dated 1st March, 2016 [new S.No.148AA] refers. Consequently, S. Nos. 148B, 148C

and 148D are being omitted.

Chapter 40:

1)

Basic Excise Duty on rubber

sheets & resin rubber sheets for soles and heels [4008 29 10] is being

reduced from 12.5% to 6%. Notification No. 12/2012-Central Excise, dated 17th

March, 2012 as amended by notification No. 12/2016-Central Excise, dated the

1st March, 2016 [new S. No 152A] refers.

Chapter 41 to 53: No change.

Chapter 54 and 55:

1)

Basic excise duty on PSF / PFY

manufactured from plastic scrap or plastic waste including waste PET bottles is

being changed from „2% without CENVAT credit or 6% with CENVAT

credit‟

to „2% without CENVAT credit or 12.5% with CENVAT credit‟. S. No. 172A of

notification No.12/2012- Central Excise, dated 17th March, 2012 as omitted by

notification No. 12/2016-Central Excise dated 1st March, 2016 refers. The rate of

12.5% will now operate through tariff.

Chapter 56 to 60: No change

Chapter 61 to 63:

1)

Basic Excise Duty of „2% (without

CENVAT credit) or 12.5% (with CENVAT credit)‟ is being imposed on readymade

garments and made up articles of textiles falling under Chapters 61, 62 and 63

(heading Nos. 6301 to 6308) of the Central Excise Tariff, except those falling

under 6309 00 00 and 6310, of retail

sale price (RSP) of Rs. 1000 and above when

they bear or are sold under a brand name. This optional levy would apply to

such readymade garments and made up

articles of textiles regardless of the composition of the garment / made up

article. However, in respect of readymade garments and made up articles of

textiles other than those mentioned above, the optional levy of Nil (without

CENVAT credit) or 6% (with CENVAT credit) in case of

garments / articles of cotton, not containing any other textile material and

Nil (without CENVAT credit) or 12.5% (with CENVAT credit) in case of garments /

made up articles of other composition, as the case may be, shall continue. S.

No. 16 of Notification No. 30/2004-CE dated the 9th July, 2004 as amended by

notification No. 15/2016-Central Excise dated the 1st March, 2016 and S. No. 7

of Notification No. 7/2012-Central Excise dated 17th March, 2012, as amended by

notification No. 7/2016-Central Excise dated the 1st March, 2016 refer.

The tariff value for readymade garments and made up

articles of textiles is also being increased from 30% to 60% which shall apply

to all goods mentioned in the notification No. 20/2001-Central Excise (N.T.)

dated 30.04.2001. Notification No. 20/2001-Central Excise (N.T.) dated

30.04.2001 as amended by Notification No. 11/2016–Central Excise (N.T) refers.

Further, the SSI exemption is being restricted for the month of March, 2016 to

Rs.12.5 lakh, subject to the condition that the turnover during financial year

2014-15 has not exceeded Rs. 4 crore. Notification No.8/2003-CE dated

01.03.2003 as amended by Notification No. 8/2016-Central Excise dated

01.03.2016 refers.

Chapter 64:

1) Abatement

rate from RSP, for all categories of footwear is being increased from 25% to

30%. S. No. 56 of Notification No. 49/2008-Central

Excise (N.T.), dated 24th December, 2008 as amended by Notification No. 12/2016-Central Excise

(N.T.), dated the 1st March, 2016 refers.

Chapter 65 to 70: No change

Chapter 71:

1)

Basic Excise Duty of 1% (without

Cenvat Credit) and 12.5% (with Cenvat Credit) is being imposed on Articles of

Jewellery [excluding articles of silver jewellery, other than those

studded

with diamonds, ruby, emerald or sapphire].

S. No. 199 of Notification No. 12/2012-

Central Excise, dated 17th March, 2012 as amended by

notification No. 12/2016-Central Excise dated 1st March, 2016 refers.

2)

SSI threshold exemption for

Articles of Jewellery [excluding articles of silver jewellery, other than those

studded with diamonds, ruby, emerald or sapphire] is being increased to Rs. 6

crore in a year, with an eligibility limit of Rs. 12 crore in the preceding

financial year. For

the month

of March, 2016, the SSI exemption for such articles of jewellery is being

restricted

to Rs. 50 lakh. Notification No. 8/2003-Central

Excise, dated 1st March, 2003 as amended by notification No. 8/2016-Central Excise dated

1st March, 2016 refers.

3)

Optional centralized registration

is being extended to manufacturers of Articles of Jewellery

[excluding articles of silver jewellery, other than

studded with diamonds, ruby, emerald or sapphire]. Notification No. 5/2016-

Central Excise (N.T.) dated 1st March, 2016 refers.

4)

Requirement of post registration

physical verification for manufacturers of Articles of Jewellery [excluding

articles of silver jewellery, other than studded with diamonds, ruby, emerald

or sapphire] is being done away with. Notification No. 35/2001-Central Excise

(N.T.), dated 26th June, 2001 is being amended suitably by notification No.

6/2016- Central Excise (N.T.) dated 1st March, 2016 refers.

5)

Basic Excise duty on Gold Bars

manufactured from gold ore or concentrate; gold dore bar and silver dore bar is

being increased from 9% to 9.5%. S. No. 189 of Notification No.12/2012- Central

Excise, dated 17th March, 2012 as amended by notification No. 12/2016- Central

Excise dated 1st March, 2016 refers.

6)

Basic Excise duty on Gold bars

and gold coins of purity not below 99.5%, produced during the process of copper

smelting is being increased from 9% to 9.5%. S. No. 191 (i) of Notification

No.12/2012- Central Excise, dated 17th March, 2012 as amended by notification

No. 12/2016- Central Excise dated 1st March, 2016 refers.

7)

Basic Excise duty on silver

manufactured from silver ore or concentrate; silver dore bar and gold dore bar

is being increased from 8% to 8.5%. S. No. 190 of Notification No.

12/2012-Central Excise, dated 17th March, 2012 as amended by notification No.

12/2016-Central Excise dated 1st March, 2016 refers.

8)

Basic Excise duty on silver in

any form, except silver coins of purity below 99.9%, produced during the

process of copper smelting is being increased from 8% to 8.5%. S. No. 191 (ii)

of Notification No. 12/2012- Central Excise, dated 17th March, 2012 as amended

by Notification No. 12/2016- Central Excise dated 1st March, 2016 refers.

9)

Basic Excise duty on silver

produced during the process of zinc or lead smelting is being increased from 8%

to 8.5%. S. No. 191A of Notification No. 12/2012- Central Excise, dated 17th

March, 2012 as amended by notification No. 12/2016-Central Excise dated 1st

March, 2016 refers.

Chapters 72 to 75: No Change.

Chapters 76:

1)

Aluminium foils of a thickness

not exceeding 0.2 mm [7607] are being notified under section 4A of the Central

Excise act for the purpose of assessment of Central Excise duty with reference

to the Retail Sale Price with an abatement of 25%. Notification No. 49/2008-

Central

Excise (N.T.) dated 21.12.2008 as amended by notification No. 12/2016-Central

Excise

(N.T.) dated 1st March, 2016 [new S. No. 64A ]

refers.

The Third Schedule to the Central Excise Act, 1944

is also being amended so as to include therein all goods falling under Chapter

heading 7607. Clause 142 (i) of the Finance Bill, 2016 refers. By virtue of

declaration under the Provisional Collection of Taxes Act, 1931, these changes

will come into force with immediate effect.

2)

The excise duty structure on

„disposable aluminium foil containers‟ is being changed from „2% without CENVAT

credit and 6% with CENVAT credit‟ to „2% without CENVAT credit and 12.5% with CENVAT credit‟. S. No. 53 of

notification No. 2/2011-Central Excise dated 01.03.2011 as amended by

notification No. 10/2016-Central Excise, dated 1st March, 2016 refers.

Chapter 77 to 83: No change.

Chapter 84 and 85:

1) Basic

Excise Duty on 5 specified parts required for the manufacture of centrifugal

pump is

being

reduced from 12.5% to 6%, subject to actual user condition. Notification No.

12/2012-

Central Excise, dated 17th March, 2012 as amended by

Notification No. 12/2016-Central Excise dated 1st March, 2016 [New S. No. 235A]

refers.

2)

Accessories of goods falling

under tariff item 8426 41 00, heading 8427, 8429 and sub-heading 8430 10 are

being included for the purposes of RSP based assessment of excise duty. S. No.

109 of Notification No.49/2008-Central Excise (N.T.), dated 24th December, 2008

as amended vide notification No.

12/2016-Central Excise (N.T.), dated 1st March, 2016 and Clause 142 (i) of the

Finance Bill, 2016 refer.

The Third Schedule to the Central Excise Act, 1944

is also being amended so as to include therein these accessories. By virtue of

declaration under the Provisional Collection of Taxes Act, 1931, this change

will come into force with immediate effect.

3)

Wrist wearable devices (commonly

known as „smart watches‟) [8517 62] are being notified for the purposes of RSP

based assessment of excise duty with an abatement of 35%.

Notification No.

49/2008-Central Excise (N.T.),

dated 21.12.2008, as

amended by

notification No. 12/2016-Central Excise (N.T.)

dated 1st March, 2016 [new S. No. 87A] refers.

The Third Schedule to the Central Excise Act, 1944

is also being amended so as to include therein such wrist wearable devices (commonly

known as „smart watches‟). Clause 142 (i) of the Finance Bill, 2016 refers. By

virtue of declaration under the Provisional Collection of Taxes Act, 1931, this

change will come into force with immediate effect.

4)

Excise duty exemption is being

withdrawn on charger/adapter, battery and wired headsets/speakers for use in

manufacture of mobile handsets including cellular phones. S. No. 272 of

Notification No. 12/2012-Central Excise, dated 17th March, 2012 as amended by

notification No. 12/2016-Central Excise dated 1st March, 2016 refers.

5)

Excise duty of „2% without CENVAT

credit / 12.5% with CENVAT credit‟ is being prescribed for charger/adapter,

battery and wired headsets/speakers, for manufacture of mobile handsets

including cellular phone, subject to actual user condition. Notification No.

12/2012-Central Excise, dated 17th March, 2012 as amended by notification

No.12/2016-Central Excise dated 1st March, 2016 [new S.Nos.263B, 263D, 263F,

263H] refers.

6)

Further, excise duty is being

exempted on inputs and parts for use in manufacture of charger/adapter, battery

and wired headsets/speakers of mobile handsets including cellular phone. Excise

duty is also being exempted on inputs and sub-parts for use in manufacture of parts of charger/adapter, battery and wired

headsets/speaker of mobile handsets including cellular phone. These exemptions

are subject to actual user condition. Notification No.12/2012-Central Excise,

dated 17th March, 2012 as amended vide notification No.12/2016-Central Excise

dated 1st March, 2016 [new S. Nos.263C, 263E, 263G, 263I] refers.

7)

Excise duty of „4% without CENVAT

credit / 12.5% with CENVAT credit‟ is being prescribed for the following

Consumer Premise Equipments (CPEs).

(i)

Routers [ tariff item 8517 69 30]

(ii)

Broadband Modems [tariff item 8517 62 30]

(iii)

Set-top boxes for gaining access to internet

[tariff item 8517 69 60]

(iv)

Reception apparatus for

television but not designed to incorporate a video display[tariff item 8528 71

00]

(v)

Digital Video Recorder

(DVR)/Network Video Recorder (NVR) [tariff item 8521 90 90]

(vi) CCTV

Camera/IP Camera [tariff item 8525 80 20]

(vii)

Lithium-ion batteries, other than

those for mobile handsets including cellular phones [tariff item 8507 60 00]

Notification No.12/2012-Central Excise, dated 17th March, 2012 as amended

by notification No.12/2016-Central Excise dated 1st March, 2016 [new

S.Nos.262A, 263J, 263L, 263N, 263P, 263R, 263T] refer.

8)

Further, excise duty is being

exempted on parts, components and accessories for use in manufacture of

Routers, broadband Modems, Set-top boxes for gaining access to internet, set

top boxes for TV, digital video recorder (DVR) / network video recorder (NVR),

CCTV camera / IP camera, lithium ion battery [other than those for mobile

handsets]. Further, Excise Duty is also being exempted on sub-parts for use in

manufacture of parts, components and accessories of the aforesaid Consumer

Premise Equipments. These exemptions are subject to actual user condition.

Notification No.12/2012-Central Excise, dated 17th March, 2012 as amended vide

notification No.12/2016-Central Excise dated 1st March, 2016 [new S. Nos.262B,

263K, 263M, 263O, 263Q, 263S, 263U] refer.

Chapter 86:

1)

Basic Excise duty on all goods

falling under 8607 (parts of railway or tramway locomotives or rolling stock)

and 8608 (railway or tramway track fixtures and fitting, etc.) is being

reduced to 6%. Notification No. 12/2012-Central

Excise as amended by notification No. 12/2016-Central Excise, dated 1st March, 2016 [new S. No.272A,

272B] refers.

2)

Basic Excise duty on refrigerated

containers [8609 00 00] is being reduced from 12.5% to

6%. Notification No. 12/2012-Central Excise as

amended by notification No.12/2016-Central Excise, dated 1st March, 2016 [new S. No. 272C]

refers.

Chapter 87:

1)

The validity period of concessional

excise duty of 6% granted to specified goods for the use in the manufacture of

electrically operated vehicles and hybrid vehicles is being extended

without time limit. First proviso to notification

No. 12/2012-Central Excise, as omitted by notification No. 12/2016 dated 1st March, 2016 refers.

2)

The description “Engine for HV

(Atkinson cycle)” appearing in S. No. 297 of notification No. 12/2012-Central

Excise is being changed to “Engine for xEV (hybrid electric vehicle)”.

Notification No. 12/2012-Central Excise as amended

by notification No. 12/2016-Central Excise, dated 1st March, 2016 refers.

3)

An Infrastructure Cess, as a duty

of excise, is being imposed on motor vehicles falling under heading 8703.

Clause 159 read with the Eleventh Schedule of the Finance Bill, 2016 refers. By

virtue of declaration under the Provisional Collection of Taxes Act, 1931, this

Cess will

come into force with immediate effect. The

effective rates of the Infrastructure Cess are being prescribed vide

notification No. 1/2016-Infrastructure Cess dated 1st March, 2016, as under:

a) Nil on :

i. Three

wheeled vehicles,

ii. Electrically

operated vehicles,

iii. Hybrid

vehicles,

iv. Hydrogen

vehicles based on fuel cell technology,

v.

Motor vehicles which after

clearance have been registered for use solely as taxi (subject to prescribed

conditions),

vi. Cars for

physically handicapped persons(subject to prescribed conditions), and

vii.

Motor vehicles cleared as

ambulances or registered for use solely as ambulance(subject to prescribed

conditions);

b)

1% on Petrol/LPG/CNG driven motor

vehicles of length not exceeding 4m and engine

capacity not exceeding 1200cc;

c)

2.5% on Diesel driven motor vehicles

of length not exceeding 4m and engine capacity

not exceeding 1500cc;

d)

4% on all categories of motor

vehicles other than those listed at (a), (b) and (c) above;

Further, the Cenvat Credit Rules are being amended

to provide that CENVAT credit cannot be utilised for payment of this

Infrastructure Cess. Further, no credit of this Cess would be available under

the Cenvat Credit Rules, 2004. Notification No.13/2016-Central Excise (N.T.)

dated 01.03.2016 refers.

4)

Accessories of certain vehicles

falling under Chapter 87 are being included for RSP based assessment. S. No.

108 of Notification No.49/2008-Central Excise (N.T.), dated 24th December, 2008

as amended vide notification

No.16/2016-Central Excise (N.T.), dated 1st March, 2016 refers. Third Schedule

to the Central Excise Act, 1944 is also being amended so as to include therein

such accessories. Clause 142(i) of the Finance Bill, 2016 refers. By virtue of

declaration under the Provisional Collection of Taxes Act, 1931, this change

will come into force with immediate effect.

Chapter 88:

1)

Excise duty on tools and tool

kits for maintenance, repair, and overhauling of aircraft is being exempted.

Further, the exemption under S.No.305 of notification No.12/2012-Central

Excise, dated 17.03.2012, is being made subject to actual user condition, along

with simplified procedure.

Chapter 89:

1)

Excise duty on Capital goods and

spare thereof, raw materials, parts, material handling equipment and consumable

for repairs of ocean-going vessels by a ship repair unit is being exempted

subject to actual user condition. New S.No.305A of notification No.12/2012-

Central Excise, dated 17.03.2012 as inserted by notification

No.12/2016-Central Excise, dated 1st March, 2016 refers.

Chapter 90 to 93: No change

Chapter 94: No change

1)

Solar lamp [tariff item 9405 50

40] is being exempted from excise duty. List-8 of Notification No.12/2012-Central

Excise, dated 17th March, 2012 as amended vide notification No.12/2016-Central

Excise dated 1st March, 2016 refers.

Chapter 95 to 96: No change.

Miscellaneous:

1) Disposable sterilized dialyzer and micro barrier [Chapter 84 or 90] of artificial kidney is being exempted from excise. Notification No.12/2012- Central Excise, dated 17.03.2012 as amended by notification No. 12/2016-Central Excise, dated 1st March, 2016 [new S. No. 315A] refers.

2) Excise duty exemption on remnant kerosene, presently available for manufacture of Linear alkyl Benzene [LAB] and heavy alkylate [HA] is being extended to N-paraffin arising in the course of manufacture of LAB and HA also. S.No.68 of notification No.12/2012- Central Excise, dated 17th March, 2012 as amended by notification No.12/2016-Central Excise, dated 1st March, 2016 refers.

3) Excise duty exemption on 5 specified items for manufacture of rotor blades and intermediates, parts and sub-parts of rotor blades for wind operated electricity generators is being withdrawn. They will now attract a concessional excise duty of 6%, for manufacture of rotor blades and intermediates, parts and sub-parts of rotor blades for wind operated electricity generators, subject to actual user condition. Notification No.12/2012-Central Excise, dated 17th March, 2012 as amended by notification No.12/2016-Central Excise dated 1st March, 2016 [New S. No.327A, List 9A] refers.

4) Basic Excise Duty on Carbon pultrusions, for manufacture of rotor blades and intermediates, parts and sub-parts of rotor blades for wind operated electricity generators, is being reduced from 12.5% to 6%, subject to actual user condition. Notification No.12/2012-Central Excise, dated 17th March, 2012 as amended vide notification No.12/2016-Central Excise dated 1st March, 2016 [New S. No. 327A, List 9A] refers.

5) Excise duty on improved cook stoves including smokeless chulhas for burning wood, agrowaste, cowdung, briquettes, and coal in being exempted unconditionally. List-8 of Notification No.12/2012-Central Excise, dated 17th March, 2012 as amended vide notification No.12/2016-Central Excise dated 1st March, 2016 [new item 22, List-8] refers. As a result, parts of such cook stoves will also be exempt from excise duty subject to actual user condition. Consequently, notification No 62/91-CE dated 25.07.1991 is rescinded by notification No 13/2016-CE dated 01.03.2016.

6) The excise duty exemption under the existing area based exemptions for production of gold and silver from gold dore, silver dore or any other raw material is being prospectively withdrawn. Thus, a new industrial unit engaged in production of refined gold from gold dore, silver dore or any other raw material, which commences commercial production on or after 1st day of March, 2016, shall not be eligible for the said excise duty exemption. Also, an existing industrial unit as on 1st of March, 2016, which undertakes substantial expansion of existing capacity or installs fresh plant, machinery or capital goods for production of gold or silver from gold dore, silver dore or any other raw material, by using such expanded capacity or such fresh plant, machinery or capital goods, and commences commercial production from such expanded capacity or such fresh plant, machinery or capital goods, on or after 1st March, 2016, shall not be eligible for the said excise duty exemption. [Amending Notifications No.5/2016 –CE dated 1.03.2016 and No.6/2016 –CE dated 1.03.2016 refers]

7) In case of power generation project based on municipal and urban waste, valid agreement between importer with urban local body for processing of municipal solid waste for not less than ten years from the date of commissioning of project is being prescribed for availing customs and excise duty concessions as an alternative to the existing condition of “production of valid power purchase agreement between the importer/producer of power and the purchaser, for the sale and purchase of electricity generated using non-conventional materials”. Notification No.33/2005- Central Excise, dated 8th September, 2005 as amended vide notification No.14/2016-Central Excise dated 1st March, 2016 refers.

8) Consequent upon abolition of the Duty Refund Procedure for exports to Nepal, notification No.8/2003-Central Excise dated 01.03.2003 is being amended so as to exclude value of clearances made for export to Nepal from the definition of „clearances for home consumption‟ under the said notification. Notification No. 8/2003-Central Excise, dated 1st March, 2003 as amended by notification No. 8/2016-Central Excise dated 1st March, 2016 refers.

COMMENTS