The taxation aspect of share transaction is very complex and thus confusing for an average taxpayer. The taxability of the same depends o...

The taxation aspect of share transaction is very complex and thus confusing for an average taxpayer. The taxability of the same depends on the holding period as well as whether the same are listed or unlisted. Tax liability will also vary depending on whether the shares have been sold on the platform of stock exchange or not. Let us try to understand all this.

- [message]

- Holding Period requirement long-term and short-term:

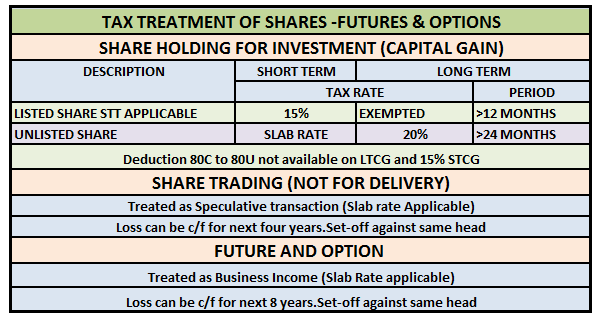

For the purpose of capital gains the shares are divided into two categories: listed and unlisted. The shares which are listed on any stock exchange shall qualify as long term once the same have been held for more than twelve months. For other shares (including shares listed on foreign stock exchanges) unlisted shares the holding period requirement is more than 24 months.

- [message]

- Tax rate for shares on which Security Transaction Tax has been paid:

For the shares which are traded on the platform of stock exchange in India the brokers are required to collect Security Transaction Tax (STT). So any profit made on the listed equity shares sold through a broker will be fully tax free if held for more than twelve months. In case of profits made on equity shares held for 12 months or less and sold on Indian stock exchanges will be taxed at a flat rate of 15.45%. Please note that on such short term capital gains the benefits of deductions under chapter VIA like section 80 C, 80 CCD, 80D, 80E, 80 G, 80GG is not available. So in case you do not have any other income except these taxable short term capital gains, you will not be able to take the benefits of various items like contribution toward public provident fund, NSC, ELSS, mediclaim premium, NPS etc. However in case your other income excluding these short-term capital gains is less than basic exemption limit, you will be entitled to take the benefit of such shortfall in the basic exemption limit while calculating your tax liability.

- [message]

- Applicable tax rate in case no STT is paid:

In case of profits made on non listed shares which were held for not more than 24 months or the listed shares on which STT was not paid and held for not more than 12 month, shall be treated like your other income and taxed at slab rate applicable to you. The long term capital gains made on such shares (listed shares held for more than 12 months and other shares held for more than 24 months) will be taxed at flat rate of 20.60%. However in case the of listed shares on which STT is not paid, you have the option to pay tax @ 10.30% without availing the benefit of indexation in case the tax liability @ 20.60 % on indexed long term capital gains is higher. It is important to note that in case the shares are not listed in India, this option of choosing between 10.30% without indexation and 20.60% indexed capital gains is not available. So in case you sell any shares which are listed on any foreign stock exchange, you will have to pay tax on long term capital gains @ 20.60% and on the short term capital gains at the slab rate applicable.

It ,may also be noted that here also you can not claim any deduction under Chapter VIA as discussed above your long term capital gains. Likewise in case your other income excluding these long-term capital gains is less than basic exemption limit, you will be entitled to take the benefit of such shortfall in the basic exemption limit here also.

- [message]

- Changes in Budget-2017

Presently Section 10(38) of the income tax act exempts capital gains which arises on sale of a equity shares listed on any stock exchange in India and held for more than 12 months and on which security Transactions Tax (STT) has been paid. This provision has been grossly misused by people for money laundering so the budget provides an additional conditions in respect of equity shares acquired after 1st October 2004, the date on which STT became applicable. The budget provides that for such shares the long term capital gains shall become exempt only if STT has been paid on purchase of such transactions as well. The government is being authorised to notify some other acquisitions on which though no STT has been paid will still continue to be exempt under Section 10(38). This notification should include the shares acquired under IPO, FPO, bonus shares, ESOPs etc. to carve out genuine transaction of acquisition of listed shares.

- [message]

- Taxation of Trading transaction

The tax treatment for transactions in shares carried out by the day traders is different than those for investors. The day traders normally indulge in transaction of shares with an intention to square off the transaction without taking the delivery of the securities. For the purpose of income tax, these transactions are treated as speculative transactions and are treated differently. For profits made on such transaction, the same has to be offered as business income and added with other income and taxed at the slab rate. In case of a few transactions the profits can be shown under the head income from other sources. Before computing the taxable amount in respect of such squared off transactions you are allowed to adjust any loss incurred by you on similar transactions. However in case the net result of such transactions in shares is net loss, you are allowed to set off such losses against other income of speculative nature only, where the transaction is squared off without taking delivery of the underlying shares/good. So any loss made by you on shares trading account can be adjusted against profits made by you for any commodity transactions.

The net speculative loss, however, is allowed to be carried forward and set off against any profit of speculative nature in four subsequent years. If the same can not be set off during this period of four years, it will lapse. In case you enter into these transaction very frequently, you will have to get your accounts audited in case the aggregate of profits and loss without netting off exceeds the threshold of Rs. 2 Core in a year.

Whether a Transaction is covered under Capital Gain or Trading in shares ,to clarify the issue , Income Tax department has released a [Income Tax circular No 04 dated 15/06/2007] [Income Tax Circular No 06 dated 29/02/2016].

Whether a Transaction is covered under Capital Gain or Trading in shares ,to clarify the issue , Income Tax department has released a [Income Tax circular No 04 dated 15/06/2007] [Income Tax Circular No 06 dated 29/02/2016].

- [message]

- Determination of Turnover in non‐ delivery based transactions /Future and Option

The ICAI has issued guidance notes for accounting treatment with a view to determine the turnover for the purpose of sec 44AB. The total of positive and negative, or favorable and unfavorable differences shall be taken as turnover.

- The total of positive and negative, or favorable and unfavorable differences shall be taken as turnover.

- Premium received on sale of options is to be included in turnover. In respect of any reverse trades entered, the difference thereon shall also form part of the turnover.

Example :Computation of Turnover Eg.

- a) Mr. X offered to purchase 5000 shares at a cost of Rs. 1000 each and also offered to sell 5000 shares at a price of Rs. 1100 each of Reliance Ltd.

- (b) He also offered to purchase 1000 shares at a cost of Rs. 3000 each and also offered to sell 1000 shares at a price of Rs. 2800 each of L&T. Thus, the turnover of Mr. X will be calculated as under:

- (i)Turnover in (a) above, Rs. 55Lacs‐ 50 Lacs = Rs. 5 Lacs

- (ii)Turnover in (b) above, Rs. 28 Lacs‐ 30 Lacs = Rs. (2 Lacs)

Thus, the net turnover of Mr X. would be (i) + (ii) = Rs. 7 Lacs.

- [message]

- Taxation of Future and Options

In case of derivative transactions of futures and options in shares, the seller and buyers generally settle the transactions with difference without taking delivery of the underlying shares, the same are still not treated as speculative and any profits/loss made on futures and options in shares will be treated as regular business income by virtue of special exclusion of such transactions from the definition of ”speculative transaction”.

In case of such transactions if the aggregate of these profits as well as loss (without netting off) exceeds Rs. 2 Crore, you will have to get your accounts audited. Any loss on such transactions can be set off against income from other sources except income from salaries.

Read more posts by [Balwant Jain] [Budget-2017] The views expressed in this article are his own

(He can be reached at jainbalwant at gmail.com and @jainbalwant)

By Balwant Jain (CA, CS and CFP)

[next]

Overview of accounting reporting and taxation

1. Overview of Accounting, Reporting and Overview of Accounting, Reporting and Taxation of Taxation of Futures, Options and other Futures, Options and other DerivativesDerivatives By: Sanjay Agarwal Founder of “Voice of CA”, NGO Email: agarwal.s.ca@gmail.com

2. Accounting aspects

3. Accounting Aspects Issues ‐ AO can not disregard accounting standards of ICAI Accounts regularly maintained in the course of business are to be taken as correct unless there are strong and sufficient reasons to indicate that they are unreliable. AO cannot disregard the method of accounting followed by the assessee where the method of accounting is based on a standard or guideline commended for adoption by a professional body such as the ICAI. Woodward Governor India (P.) Ltd. vs CIT [2009] 179 TAXMAN 326 (SC) CIT vs Virtual Soft Systems Ltd. [2012] 18 taxmann.com 119 (Delhi) Jt CIT vs K. Raheja (P.) Ltd. [2006] 102 ITD 414 (Mum.‐ Trib.)

4. Notified Accounting Standards by central government (Till date) under section 145 of income tax act, 1961 A. Accounting Standard I ‐ relating to disclosure of accounting policies. B. Accounting Standard II ‐ relating to disclosure of prior period and extraordinary items and changes in accounting policies

5. Draft Tax Accounting Standards Drafts of the Tax Accounting Standards on the following issues based on the corresponding Accounting Standard issued by the ICAI after harmonising the same with the provisions of the Act S. No. TAS Corresponding AS 1. Disclosure of Accounting Policies AS‐1 2. Valuation of Inventories AS‐2 3. Events Occurring After the Previous Year AS‐4 4. Prior Period Expense AS‐5 5. Construction Contracts AS‐7 6. Revenue Recognition AS‐9 7. Accounting for Tangible Fixed Assets AS‐10

6. Draft Tax Accounting Standards S. No. TAS Corresponding AS 8. The Effects of Changes in Foreign Exchange Rates AS‐11 10. Securities AS‐13 11. Borrowing Costs AS‐16 12. Leases AS‐19 13. Intangible Assets AS‐26 14. Provisions, Contingent Liabilities and Contingent Assets AS‐29 Contd…

7. Accounting standards V. Tax Accounting Standards ‐ In respect of Derivatives Accounting standards by ICAI TAS ‐ 1 The mark‐to‐market gain/ loss or an expected gain/ loss should be recognized in the statement of Profit and Loss as per AS– 30, para 99(a) (Derivative Hedging instrument at fair value). As per TAS on Accounting Policies The mark‐to‐market loss or an expected loss (except those covered by other TAS) shall not be recognized.

8. Accounting Standards issued by ICAI ‐In respect of Financial Instruments including derivatives

9. Contd…

10. AS‐30 issued by ICAI The objective of this Standard is to establish principles for recognising and measuring financial assets, financial liabilities and some contracts to buy or sell non‐financial items. Requirements for presenting information about financial instruments are in Accounting Standard (AS) 31, Financial Instruments: Presentation. Requirements for disclosing information about financial instruments are in Accounting Standard (AS) 32

11. Contd….

12. AS – 31‐ Presentation of financial instruments Objective: To establish principles for presenting financial instruments as Liabilities or Equity, and for off‐setting financial assets and financial liabilities. Scope: 1. Classification of Financial instruments, from the perspective of the issuer, into financial assets, financial liabilities and equity instruments. 2. Classification of related interest, dividends, losses and gains. 3. Circumstances in which financial assets and financial liabilities should be offset.

13. AS – 32‐ Disclosure of financial instruments The objective of this Standard is to establish principles for presenting financial instruments as liabilities or equity and for offsetting financial assets and financial liabilities. It applies to the classification of financial instruments, from the perspective of the issuer, into financial assets, financial liabilities and equity instruments; the classification of related interest, dividends, losses and gains; and the circumstances in which financial assets and financial liabilities should be offset.

14. Reporting aspects Reporting aspects

15. Determination of turnover in non‐ delivery based transactions The ICAI has issued guidance notes for accounting treatment with a view to determine the turnover for the purpose of sec 44AB. The total of positive and negative, or favorable and unfavorable differences shall be taken as turnover.

16. Guidance on accounting treatment Premium received on sale of options is to be included in turnover. In respect of any reverse trades entered, the difference thereon shall also form part of the turnover.

17. Tax Audit In case a lot of transactions are executed in routine, then it can be held as an adventure in the nature of trade and profit or loss from such a business will be covered under the head PGBP. In case of derivatives of securities the profit/ loss is not treated as speculative. Moreover, it is said to be non‐ speculative.

18. Tax Audit However, in case of commodity transactions, it shall be considered as speculative, if the same is not for the purpose of hedging (upto AY 2013‐ 14). As per sec clause (e) of 43(5) of the Income Tax Act, 1961, commodity transactions shall be considered as non‐speculative, from AY 2014‐ 15 as per the amended Finance Act 2013

19. Computation of turnover Eg.

a) Mr. X offered to purchase 5000 shares at a cost of Rs. 1000 each and also offered to sell 5000 shares at a price of Rs. 1100 each of Reliance Ltd.

(b) He also offered to purchase 1000 shares at a cost of Rs. 3000 each and also offered to sell 1000 shares at a price of Rs. 2800 each of L&T. Thus, the turnover of Mr. X will be calculated as under:

(i)Turnover in (a) above, Rs. 55Lacs‐ 50 Lacs = Rs. 5 Lacs

(ii)Turnover in (b) above, Rs. 28 Lacs‐ 30 Lacs = Rs. (2 Lacs)

Thus, the net turnover of Mr X. would be (i) + (ii) = Rs. 7 Lacs.

20. Taxation aspects

21. MAJOR ISSUES…… Whether the derivative transaction is a speculative transaction? Taxability‐ whether as business income or capital gains? Whether set off of losses from derivative transactions is possible?

22. Taxation aspects Key Points No specific provision under the Act regarding taxability of

derivatives. Provisions having an indirect bearing on derivative transactions are Section 28, sec. 73(1) and sec.43(5). The presentation and disclosure of derivatives in financial statements is required by ‘AS‐31 and 32’ respectively issued by ICAI.

23. Speculation transaction as per Sec 43(5) of IT Act Speculative transaction means a transaction in which a contract for the purchase or sale of any commodity including stock and shares, is periodically or ultimately settled otherwise than by actual delivery or transfer of commodity or scrips. Contd…

24. Provisions to Sec 43(5) Transactions not to be deemed as speculative : (a) a contract in respect of raw materials or merchandise entered into by a person in the course of his manufacturing or merchanting business to guard against loss through future price fluctuations in respect of his contracts for actual delivery of goods manufactured by him or merchandise sold by him, or Contd…

25. (b) a contract in respect of stocks and shares entered into by a dealer or investor therein to guard against loss in his holdings of stocks and shares through price fluctuations, or (c) a contract entered into by a member of a forward market or a stock exchange in the course of any transaction in the nature of jobbing or arbitrage to guard against loss which may arise in the ordinary course of his business as such member, or Contd… Provisions to Sec 43(5)

26. (d) an eligible transaction in respect of trading in derivatives referred to in clause (ac) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956) carried out in a recognized stock exchange. Eligible transactions on BSE and NSE w.e.f. 25th Feb 2006 shall not be considered as speculative vide Notification No. 2/2006, dated 25‐1‐2006 of Income Tax Act, 1961. Contd… Provisions to Sec 43(5)

27. Derivatives As per clause (ac), of sec 2 of Securities Contract (Regulations) Act, 1956, Derivatives include :‐ (a) a security derived from a debt instrument, share, loan, whether secured or unsecured, risk instrument or contract for differences or any other form of security. (b) a contract which derives its value from the prices, or index of prices, of underlying securities. The definition of derivatives earlier rederred to in clause (aa) was re‐lettered as clause (ac), of sec 2 of Securities Contracts (Regulations) Act, 1956 vide Circular no. 14/2006, Dated 28‐12‐2006 of the Income Tax Act, 1961. Accordingly, the amendment has been done in clause (5) of section 43 of the Income Tax Act, 1961.

28. Explanation ‐ Eligible transaction A) carried out electronically on screen‐based systems through a stock broker or sub‐broker or such other intermediary registered u/s 12 of the SEBI Act, 1992 (15 of 1992) in accordance with the provisions of the SC(R)A, 1956 (42 of 1956) or the SEBI Act, 1992 (15 of 1992) or the Depositories Act, 1996 (22 of 1996) and the rules, regulations or bye‐laws made or directions issued under those Acts or by banks or mutual funds on a recognized stock exchange; and

29. Explanation ‐ Eligible transaction (B) which is supported by a time stamped contract note issued by such stock broker or sub‐broker or such other intermediary to every client indicating in the contract note the unique client identity number allotted under any Act referred to in sub‐clause (A) and permanent account number allotted under this Act;

30. Explanation‐ Recognized Stock Exchange A recognized stock exchange as referred to in clause (f) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956) and which fulfils such conditions as may be prescribed and notified by the Central Government for this purpose. BSE and NSE as recognized stock exchanges.

31. Amendments as in Finance Bill, 2013 As passed by Lok Sabha‐ Insertion of clause (5) in the proviso, w.e.f. 1st day of April 2014. Clause(e)‐ “An eligible transaction in respect of trading in commodity derivatives carried out in a recognized association”

32. Amendments as in Finance Bill, 2013 Explanation shall be renumbered as “Explanation 1” thereof and in the Explanation 1 as so renumbered, for the words “this clause” the word, brackets and letter “clause (d)” shall be substituted.

33. Amendments as in Finance Bill, 2013 Explanation 2 for the purposes of clause (e), the expressions – Commodity derivatives: shall have the meaning as assigned to it in Chapter VII, of the Finance Act, 2013 (i.e. Commodities Transaction Tax). Contd…

34. Explanation 2 “Eligible transaction”: Means any transaction‐ (A) carried out electronically on screen‐based systems through member or an intermediary, registered under the bye‐laws, rules and regulations of the recognized association for trading in commodity derivatives in accordance with the provisions of the Forward Contracts (Regulation) Act, 1952 and the rules, regulations or bye‐ laws made or directions issued under that Act on a recognized association; and Contd… Amendments as in Finance Bill, 2013

35. Amendments as in Finance Bill, 2013 Explanation 2 (B) which is supported by a time stamped contract notes issued by such member of intermediary to every client indicating in the contract note, the unique client identity number allotted under the Act, rules, regulations or bye‐ laws referred to in sub‐clause (A), unique trade number and permanent account number allotted under this Act; Contd…

36. Amendments as in Finance Bill, 2013 Explanation 2 “Recognized association” means a recognized association as referred to in clause (j) of section 2 of the Forward Contracts (Regulation) Act, 1952 and which fulfils such conditions as may be prescribed and is notified by the Central Government for this purpose.’ Contd…

37. Capital Gain vs. Business income As per section 2(14) of the Act, ‘capital asset’ means property of any kind held by an assessee, whether or not connected with his business or profession. Derivatives are security defined under SC( R) Act or the contracts carrying right, thus they can be considered as a property carrying value.

38. Tax treatment in brief Non‐corporate assessee Investor‐taxability under capital gains Businessman‐ i) if actual delivery, under PGBP ii) if no actual deliver, speculation (sec. 43) Corporate assessee Investor‐ taxability under capital gains Businessman‐ i) If actual delivery: * If banking co. regarding shares‐ NormalPGBP (expl. To sec. 73) * Any co. regarding any other commodity‐NormalPGBP Other Co. regarding shares‐ Speculation (expl.sec. 73) ii)If no actual delivery‐ speculation (sec. 43)

39. Set off of speculation losses‐Sec 73 of IT Act, 1961 1) Any loss, computed in respect of a speculation business carried on by the assessee, shall not be set off except against profits and gains, if any, of another speculation business. 2) Where for any assessment year any loss computed in respect of a speculation business has not been wholly set off under sub‐section (1), so much of the loss as is not so set off or the whole loss where the assessee had no income from any other speculation business, shall, subject to the other provisions of this Chapter, be carried forward to the following assessment year, and—

40. (i) it shall be set off against the profits and gains, if any, of any speculation business carried on by him assessable for that assessment year; and (ii) if the loss cannot be wholly so set off, the amount of loss not so set off shall be carried forward to the following assessment year and so on. Contd… Set off of speculation losses‐Sec 73 of IT Act, 1961

41. (3) In respect of allowance on account of depreciation or capital expenditure on scientific research, the provisions of sub‐section (2) of section 72 shall apply in relation to speculation business as they apply in relation to any other business. (4) No loss shall be carried forward under this section for more than four assessment years immediately succeeding the assessment year for which the loss was first computed (vide Circular no. 3/2006 dated 27.02.2006 w.e.f. AY 2006‐07). Contd… Set off of speculation losses‐Sec 73 of IT Act, 1961

42. Explanation.—Where any part of the business of a company [other than a company whose gross total income consists mainly of income which is chargeable under the heads "Interest on securities", "Income from house property", "Capital gains" and "Income from other sources"], or a company the principal business of which is the business of banking or the granting of loans and advances) consists in the purchase and sale of shares of other companies, such company shall, for the purposes of this section, be deemed to be carrying on a speculation business to the extent to which the business consists of the purchase and sale of such shares. Contd… Set off of speculation losses‐Sec 73 of IT Act, 1961

43. Clarification for carry forward of speculative losses The loss in respect of speculation business shall be allowed to carried forward for four years in place of eight years vide Circular no. 3/2006, dated 27.02.2006. Finance Act, 2005 has amended the said sub‐section (4) so as to reduce the period of loss to be carried forward from eight assessment years to four assessment years. Applicability: From A.Y. 2006‐07 onwards.

44. Issues…… Whether transaction in an exchange before the release of notification would amount to speculation? No, the notification is only clarificatory in nature, therefore, the transaction would not be considered as speculative. ACIT, Vs. Arnav Akshay Mehta [2012] 25 taxmann.com 252 (ITAT ‐ Mum.) ACIT, Vs. Vimal Vadilal Shah [2012] 27 taxmann.com 197 (ITAT – Ahm.)

45. Issues…… Whether mere violation w.r.t. to fulfillment of conditions of invoice and contract would amount to speculation? Mere intention of law was that the transactions to be carried out through recognized stock exchange and hence, not to be considered as speculative. Vibha Goel Vs. JCIT, [2012] 25 taxmann.com 142 (ITAT – Chandigarh)

46. Issues If actual delivery of share scrips does not take place both for purchases as well as sales – Sec 43(5) – delivery recalled by brothers – No actual delivery. Speculative transation – Loss cannot be set off against business income. ACIT Vs. Claytone Commercial Co. Ltd. (ITAT, Delhi) 67 ITD 118 Ram Lal & Sons Vs. ITO (ITAT, Asr) 71 ITD 256

47. Other Issues……. Whether derivatives transactions not settled through delivery of the asset would be considered as speculative? Derivatives transactions (not a commodity derivative) through a recognized stock exchanged shall not be speculative. [Dy. CIT v. Paterson Securities (P.) Ltd. [2010] 127 ITD 386 (Chennai)]

48. Speculative business income Explanation 2 of Sec 28 of Income Tax Act, 1961‐ Where speculative transactions carried on by an assessee are of such a nature as to constitute a business, the business (hereinafter referred to as "speculation business") shall be deemed to be distinct and separate from any other business.

49. Tax treatment for derivative transactions

50. Recapitulation

51. Speculative transactions…….. Intra‐day trading shall be considered as speculation business transactions and the income there from would be either speculation gains or losses. However, if based the on facts and circumstances of your case, you can prove that though delivery was not actually taken it was within your normal business transaction, it could be treated as non‐ speculation business income.

52. Taxability of speculative transactions Income from speculation gains is taxed at the normal rates. Speculation losses can be set off only against speculation gains as per sec 73. Trading in derivatives (futures and options) is treated as non‐speculation business even though delivery is not effected in such transactions.

53. Taxability of speculative transactions Speculation losses can be carried forward for a maximum of four years immediately succeeding the relevant assessment year vide Circular no. 3/2006, dated 27.02.2006 of Income Tax Act, 1961. Considering the fact, the physical existence of money, currency can be considered as a commodity. Contd…

54. Taxability of speculative transactions Therefore, currency derivatives transactions shall be covered by main part of the speculative transactions definition. However, there have been different decisions of various Tribunals of considering currency derivatives transactions as commodity and non‐ commodity transactions. Contd…

55. Taxability of speculative transactions Also, currency derivatives are transacted at stock exchanges and not on commodity exchanges. Therefore, should not be considered as speculative transactions, if they qualify as derivatives under SCRA, 1956. Contd…

56. Taxability of speculative transactions Currency transactions on stock exchanges, indicates them to be a type of securities. Therefore, qualify for treatment as security derivatives (non‐speculative). Contd…

57. Speculative transactions Since, the income from speculative transactions is considered as business income, Audit would be required if the turnover exceeds 2 crore. Sale value of the transaction shall be considered for the purpose of calculation of turnover. Contd…

58. Provisions of Sec 44AD to have impact In respect of loss from non‐delivery of transactions such as F&O and derivatives. It mandates disclosure of at least 8% of net profit on gross turnover and if not, books of accounts are required to be maintained. There is no clear cut guidelines, as to whether assessee w.r.t. to derivatives transaction, can use the provision of this section or not.

59. For any queries, feel free to contact: CA Sanjay Agarwal Founder of “Voice of CA” Email id : agarwal.s.ca@gmail.com Assisted by : Pallav Agarwal

[next]

[next]

Distinction between shares held as stock-in-trade and shares held as investment - tests for such a distinction

CIRCULAR NO. 4/2007, DATED 15-6-2007

The Income Tax Act, 1961 makes a distinction between a "capital asset" and a "trading asset".

2. Capital asset is defined in Section 2(14) of the Act. Long-term capital assets and gains are dealt with under Section 2(29A) and Section 2(29B). Short-term capital assets and gains are dealt with under Section 2(42A) and Section 2(42B).

3. Trading asset is dealt with under Section 28 of the Act.

4. The Central Board of Direct Taxes (CBDT) through Instruction No.1827 dated August 31, 1989 had brought to the notice of the assessing officers that there is a distinction between shares held as investment (capital asset) and shares held as stock-in-trade (trading asset). In the light of a number of judicial decisions pronounced after the issue of the above instructions, it is proposed to update the above instructions for the information of assessees as well as for guidance of the assessing officers.

5. In the case of Commissioner of Income Tax (Central), Calcutta Vs Associated Industrial Development Company (P) Ltd (82 ITR 586), the Supreme Court observed that:

"Whether a particular holding of shares is by way of investment or forms part of the stock-in-trade is a matter which is within the knowledge of the assessee who holds the shares and it should, in normal circumstances, be in a position to produce evidence from its records as to whether it has maintained any distinction between those shares which are its stock-in-trade and those which are held by way of investment."

6. In the case of Commissioner of Income Tax, Bombay Vs H. Holck Larsen (160 ITR 67), the Supreme Court observed :

"The High Court, in our opinion, made a mistake in observing whether transactions of sale and purchase of shares were trading transactions or whether these were in the nature of investment was a question of law. This was a mixed question of law and fact."

7. The principles laid down by the Supreme Court in the above two cases afford adequate guidance to the assessing officers.

8. The Authority for Advance Rulings (AAR) (288 ITR 641), referring to the decisions of the Supreme Court in several cases, has culled out the following principles :-

"(i) Where a company purchases and sells shares, it must be shown that they were held as stock-in-trade and that existence of the power to purchase and sell shares in the memorandum of association is not decisive of the nature of transaction;

(ii) the substantial nature of transactions, the manner of maintaining books of accounts, the magnitude of purchases and sales and the ratio between purchases and sales and the holding would furnish a good guide to determine the nature of transactions;

(iii) ordinarily the purchase and sale of shares with the motive of earning a profit, would result in the transaction being in the nature of trade/adventure in the nature of trade; but where the object of the investment in shares of a company is to derive income by way of dividend etc. then the profits accruing by change in such investment (by sale of shares) will yield capital gain and not revenue receipt".

9. Dealing with the above three principles, the AAR has observed in the case of Fidelity group as under:-

"We shall revert to the aforementioned principles. The first principle requires us to ascertain whether the purchase of shares by a FII in exercise of the power in the memorandum of association/trust deed was as stockin-trade as the mere existence of the power to purchase and sell shares will not by itself be decisive of the nature of transaction. We have to verify as to how the shares were valued/held in the books of account i.e. whether they were valued as stock-in-trade at the end of the financial year for the purpose of arriving at business income or held as investment in capital assets. The second principle furnishes a guide for determining the nature of transaction by verifying whether there are substantial transactions, their magnitude, etc., maintenance of books of account and finding the ratio between purchases and sales. It will not be out of place to mention that regulation 18 of the SEBI Regulations enjoins upon every FII to keep and maintain books of account containing true and fair accounts relating to remittance of initial corpus of buying and selling and realizing capital gains on investments and accounts of remittance to India for investment in India and realizing capital gains on investment from such remittances. The third principle suggests that ordinarily purchases and sales of shares with the motive of realizing profit would lead to inference of trade/adventure in the nature of trade; where the object of the investment in shares of companies is to derive income by way of dividends etc., the transactions of purchases and sales of shares would yield capital gains and not business profits."

10. CBDT also wishes to emphasise that it is possible for a tax payer to have two portfolios, i.e., an investment portfolio comprising of securities which are to be treated as capital assets and a trading portfolio comprising of stock-in-trade which are to be treated as trading assets. Where an assessee has two portfolios, the assessee may have income under both heads i.e., capital gains as well as business income.

11. Assessing officers are advised that the above principles should guide them in determining whether, in a given case, the shares are held by the assessee as investment (and therefore giving rise to capital gains) or as stock-in-trade (and therefore giving rise to business profits). The assessing officers are further advised that no single principle would be decisive and the total effect of all the principles should be considered to determine whether, in a given case, the shares are held by the assessee as investment or stock-in-trade.

12. These instructions shall supplement the earlier Instruction no. 1827 dated August 31, 1989.

(F.No.149/287/2005-TPL)

COMMENTS